T-Bills vs High-Yield Savings for Short-Term Cash

Compare Treasury Bills and High-Yield Savings Accounts for safer, smarter short-term cash management.

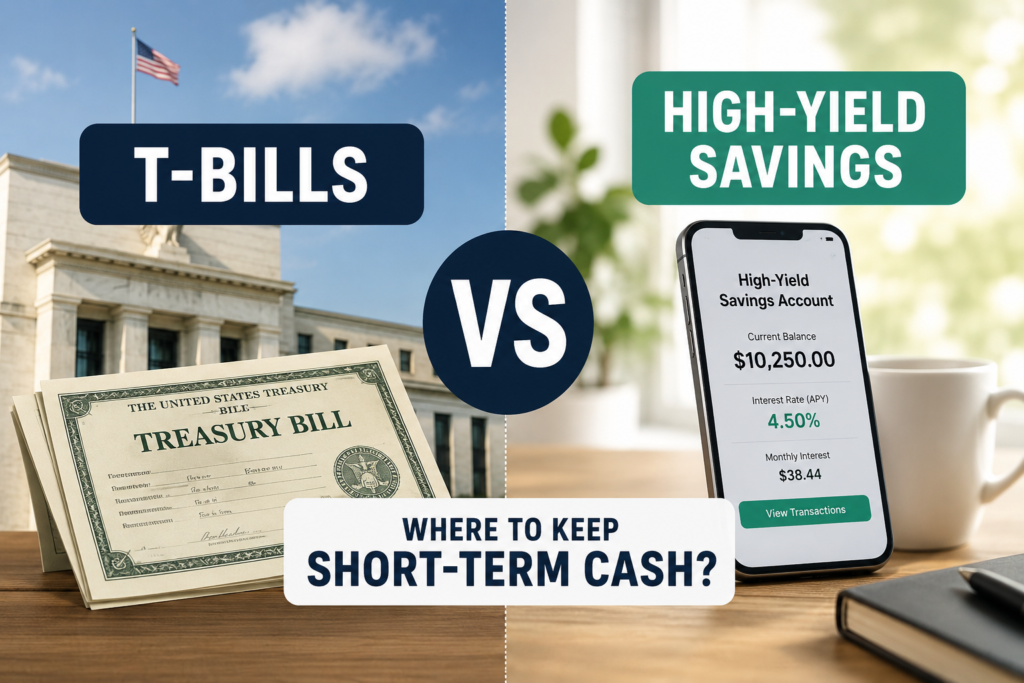

Treasury Bills vs High-Yield Savings: Best Place for Short-Term Cash

Treasury Bills vs High-Yield Savings: Where Should You Keep Short-Term Cash?

Is your money working… or just lounging on the couch doing absolutely nothing?

If you’re an American with cash set aside for the next few months — maybe for a home down payment, a vacation, an emergency fund, or money waiting for the right opportunity — you’ve probably asked yourself the classic question:

Treasury Bills vs High-Yield Savings: which one actually makes more sense?

It’s kind of like choosing between:

Treasury Bills

The Reliable Government Employee- ✔ Predictable, locked-in rates

- ✔ Exempt from state/local taxes

- ✖ Money is locked until maturity

High-Yield Savings

The Flexible Modern Freelancer- ✔ Instant access to your cash

- ✔ Takes 5 minutes to set up

- ✖ Rates can drop at any time

Both are safe. Both earn interest. Both sound boring at first.

But one of them could quietly put more money in your pocket depending on your goal.

Let’s get straight to it.

First: What Are Treasury Bills?

Treasury Bills — or simply T-Bills — are short-term debt securities issued by the U.S. government.

In plain English: 🦅 You’re lending money to the United States.

And let’s be honest…

If the U.S. government collapses, your investment returns will probably be the least of your concerns.

T-Bills come with short maturity periods:

📅 4 weeks

📅 8 weeks

📅 13 weeks

📅 17 weeks

📅 26 weeks

📅 52 weeks

You buy them at a discount and receive the full face value when they mature.

Example:

💵 Buy for $9,750

💵 Receive $10,000 later

Your profit is the difference.

Simple. No confusing banking tricks.

Visually, it works like this:

How the T-Bill Discount Works

The $250 difference is your profit. Simple. No confusing banking tricks.

The Treasury basically says: “Thanks for the loan. Here’s your money back with a little bonus.”

Clean. Efficient. Very American.

What Is a High-Yield Savings Account?

Think of it as savings… but upgraded.

Unlike traditional bank savings accounts that offer laughably low rates like 0.01% APY (which is basically a polite insult), High-Yield Savings Accounts offer much stronger returns.

Today, many U.S. online banks offer competitive rates.

Example:

🏦 Deposit $10,000

📈 Interest appears automatically

🔓 Withdraw whenever you want

No lock-up period. No Treasury auctions. No maturity dates.

Just: Deposit and chill.

For many people, that convenience alone wins the argument.

Because simplicity has value too.

The Showdown: Treasury Bills vs High-Yield Savings

Let’s settle this.

🥊 The Official Scorecard

Click a round to see why

Round 1: Yield 🏆 T-Bills

Round 2: Liquidity 🏆 High-Yield Savings

Round 3: Taxes 🏆 T-Bills

Round 4: Simplicity 🏆 High-Yield Savings

Round 5: Predictability 🏆 T-Bills

So… Who Wins?

It depends on who you are. Classic finance answer. Still true.

Choose T-Bills If You:

✔ Don’t need immediate access

✔ Want predictable returns

✔ Live in a high-tax state

✔ Want to maximize yield

✔ Don’t mind a little setup hassle

Your personality type:

🧠 “Spreadsheet enthusiast who gets excited about optimizing 0.35%” Respect.

Choose High-Yield Savings If You:

✔ Want instant access

✔ Hate unnecessary complexity

✔ Prefer convenience

✔ Are building an emergency fund

Your personality type:

😌 “I want peace, returns, and zero drama.”

Also respectable.

What If You Use Both?

Plot twist:

This might actually be the smartest move.

Split your money like this:

Emergency cash

→ High-Yield Savings

(For real emergencies: car trouble, medical bills, surprise travel)

Planned short-term money

→ T-Bills

(Example: home down payment in 8 months)

This gives you:

⚡ Liquidity

📈 Optimized returns

🛡 Safety

The best of both worlds.

Like having cake and eating it too.

Still not sure why people say that, but here we are.

A Real Example

🎛️ The “Best of Both Worlds” Allocator

Assume you have $20,000. Move the slider to build your perfect strategy.

Balanced: You have a solid emergency buffer and optimized yield.

Let’s say you have $20,000.

Split it like this: $8,000 in High-Yield Savings. Instant access.

$12,000 in rolling 13-week T-Bills

Better yield.

Result: Your money works in shifts.

Part stays on standby. Part works overtime.

It’s basically a small business.

Without HR meetings.

The Mistake Many Americans Still Make

🛑 The "Lazy Money" Trap

If you leave $25,000 sitting in a traditional bank account (0.05%) instead of moving it to a T-Bill or HYSA (4.8%) for one year...

- A round-trip international flight ✈️

- A brand new iPhone 📱

- A highly suspicious amount of takeout 🍔

So Which One Is Better?

If you want maximum efficiency:

Treasury Bills: If you want maximum convenience:

High-Yield Savings: If you want balance:

Use both For many Americans managing short-term cash, this is the smartest strategy.

Because personal finance is rarely about finding one perfect product.

It’s about matching the tool to your goal.

Your timeline.

Your comfort level.

Your priorities.

Final Verdict on Treasury Bills vs High-Yield Savings

There’s no bad option here.

Both are excellent.

The real enemy is leaving your money parked in a near-zero-interest account while inflation throws a party.

If your short-term cash is just sitting there:

Do something with it.

Today.

Your future self will thank you.

And honestly?

Few things feel better than making money while you sleep.

Related content

Open Enrollment Budget Checklist Tips

Plan smarter health benefits and payroll costs with practical open enrollment budgeting tips for U.S. workers.

Keep reading * You will remain on the current websiteI have been a content producer for over 10 years, specializing in online writing across a wide range of topics—particularly finance, health, and human behavior. I’m an expert in SEO-driven writing and cultural research.