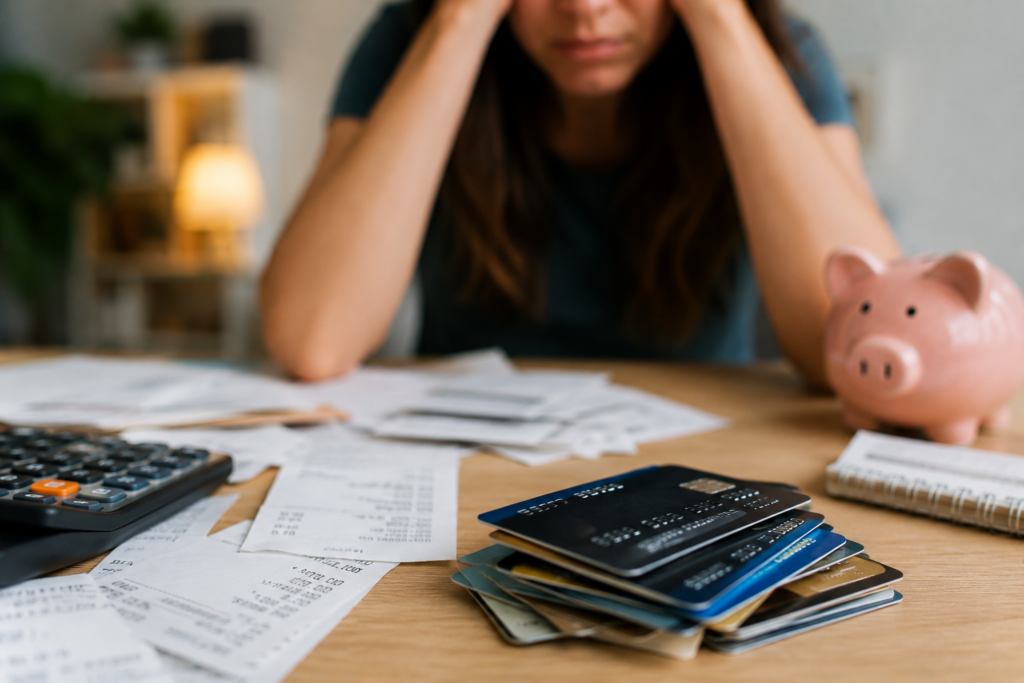

The Real Problem With 0% APR Balance Transfer Fees

Learn how 0% APR balance transfer fees can quietly increase debt and ruin your payoff strategy.

The Math Behind a Seemingly Cheap Offer

A 0% APR balance transfer offer feels a lot like finding fries at the bottom of the bag. Unexpected. Beautiful. Financially emotional.

Then the fee hits.

Suddenly, that “smart money move” starts looking like a gym membership you forgot to cancel.

Welcome to the real world of 0% APR Balance Transfer Fees — where credit card companies technically tell the truth, but definitely hope you never open the calculator app.

The Ad Says “0% APR” 😍

“FREE MONEY.”

“There’s a 3% to 5% transfer fee waiting behind the curtain.”

And yes, that matters more than most people think.

Before the “saving money” part even starts.

Why Credit Card Companies LOVE Balance Transfers

Because they know consumers see: 0% and mentally stop reading.

A balance transfer offer is basically the financial version of: “Free trial!” (until your card gets charged 11 minutes later).

Banks make money from:

- transfer fees

- late payments

- deferred interest

- people missing the payoff deadline

- customers continuing to spend on the card

The fee itself is often the appetizer.

The real profit comes later.

The Sneaky Math Nobody Talks About

Let’s compare two situations.

⚖️ The Balance Transfer Showdown

Option A: Keep Existing Debt

- Balance: $6,000

- APR: 22%

- Payoff timeline: 18 months

Option B: Transfer to 0% Card

- Intro APR: 0% for 15 months

- Transfer Fee: 5%

Sounds better, right? Maybe.

Because if you DON’T pay the balance before the promo ends…

🚨 BOOM.

The regular APR activates. And many cards jump straight to:

The leftover balance suddenly becomes expensive again. That’s how a “smart financial strategy” quietly turns into a debt treadmill.

The Biggest Mistake Americans Make

People focus on: “How much can I transfer?”

Instead of: “Can I realistically pay this off in time?”

That’s the real question.

A balance transfer only works if:

- you stop adding new debt

- your monthly payments are aggressive enough

- the timeline is realistic

Otherwise, you’re basically moving debt from one kitchen drawer to another.

Cleaner drawer. Same mess.

The Psychology Trap

A 0% APR offer creates emotional relief. That’s powerful.

People suddenly feel:

- safer

- less stressed

- “ahead”

- back in control

And that emotional reset can accidentally create new spending.

Example:

“Well… my old card is empty now.”

Dangerous sentence.

Because many borrowers:

- transfer the balance

- free up old credit cards

- start spending again

- now owe debt in TWO places

That’s how consolidation becomes multiplication.

The “Minimum Payment” Illusion

Here’s another trick.

Your new minimum payment often looks:

Which feels amazing.

Until you realize: small minimum payments can make it mathematically impossible to finish before the promotional window closes.

💰 $667 /mo

What you actually need to pay😌 $120 /mo

Guarantees you miss the deadlineThe bank isn’t trying to help you escape debt quickly.

The bank is trying to keep you profitable.Balance Transfers Are Tools — Not Miracles

This is important.

0% APR Balance Transfer Fees are not automatically bad.

Sometimes they absolutely make sense.

A 3% fee can save thousands in interest if:

- the debt is large

- payoff timing is realistic

- spending stops immediately

That’s a smart use case.

But many Americans treat balance transfers like a financial reset button.

They’re not. They’re more like refinancing chaos.

Helpful? Potentially. Dangerous if used emotionally? Absolutely.

When a Balance Transfer Actually Makes Sense

✅ Good Scenario

You:

- have stable income

- already cut unnecessary spending

- built a payoff plan

- can eliminate the balance during the promo window

That’s ideal.

The fee becomes a calculated cost.

Like paying for moving boxes during a cheaper apartment move.

When It’s Probably a Bad Idea

🚩 Red Flags

You:

- keep relying on credit cards monthly

- don’t know how much you can realistically pay

- want “breathing room” without behavior changes

- already missed payments recently

- plan to continue carrying balances long-term

In those situations, the transfer fee may simply delay the real problem.

And delayed financial problems usually return stronger.

Like raccoons.

Why This Matters More in America Right Now

The U.S. credit card market runs heavily on revolving debt.

Millions of Americans carry balances month to month while:

- interest rates stay elevated

- living costs remain stubbornly high

- emergency savings stay weak

So balance transfer offers feel attractive because they promise: temporary relief.

But temporary relief is not the same thing as financial recovery.

That distinction matters. Especially when fees get ignored during the decision-making process.

The “Best Balance Transfer Card” Myth

Financial websites love publishing: “BEST 0% APR CARDS OF THE YEAR”.

What they don’t emphasize enough:

- transfer fee percentages vary

- intro periods vary

- approval odds vary

- some cards charge deferred interest-style penalties indirectly

- high credit scores usually get the best terms

Meaning: the deal advertised online may not be the deal you personally receive.

That’s why reading the fine print matters more than flashy APR marketing.

The Smart Way to Evaluate a Balance Transfer

Before transferring anything, ask:

🔍 The Pre-Transfer Audit

Ask yourself these 5 questions before moving any debt.

The Hidden Cost Isn’t Always the Fee

The real danger of 0% APR Balance Transfer Fees isn’t necessarily the upfront percentage.

It’s the false confidence they create.

The transfer can make people feel financially healthier before they actually are.

That emotional gap leads to:

- overspending

- delayed budgeting

- ignoring payoff timelines

- carrying balances longer

And that’s where the expensive damage happens.

A Better Way to Think About It

Instead of asking:“Should I transfer this debt?”

Ask: “Am I ready to aggressively eliminate this debt?”

Completely different mindset.

One is passive. One is active.

And balance transfers only work well when paired with aggressive repayment behavior.

The Fast-Food Combo Version of Debt

🍔 The “Diet Soda” Delusion

Is like ordering a Diet Soda…

Large fries, double cheeseburger, extra nuggets & a chocolate shake.

That’s what happens when people transfer balances without fixing:

The APR changes. The habits don’t.

“And habits are usually the real interest rate.”

The Best Use of a 0% APR Offer

The strongest strategy is surprisingly boring.

Here’s what financially disciplined borrowers do:

✅ The Balance Transfer Success Protocol

Check off each step to guarantee you beat the debt

That’s it.

Just math and consistency.

Related content

T-Bills vs High-Yield Savings for Short-Term Cash

Compare Treasury Bills and High-Yield Savings Accounts for safer, smarter short-term cash management.

Keep reading * You will remain on the current website T-Bills vs High-Yield Savings for Short-Term Cash

Keep reading You will remain on the current websiteI have been a content producer for over 10 years, specializing in online writing across a wide range of topics—particularly finance, health, and human behavior. I’m an expert in SEO-driven writing and cultural research.