Do You Need Umbrella Insurance? A Simple, Honest Guide

Learn how umbrella insurance works, costs, and when it protects your assets beyond standard coverage.

Umbrella Insurance: Is It Necessary or Just Extra?

If you live in the United States, have car insurance and maybe homeowners insurance, you probably think you’re protected.

And technically, you are — up to a point.

The problem is that this “point” is usually something like $300k to $500k in coverage.

And in the real world of the U.S.… that’s not as much as it sounds.

Now pay attention to this:

- A serious accident with injuries can easily exceed $500k+

- Lawsuits can go over $1 million

- Medical and legal costs escalate very quickly

And your basic insurance has a limit.

The rest? Becomes your problem.

Let’s break it down.

What is umbrella insurance (no fluff)

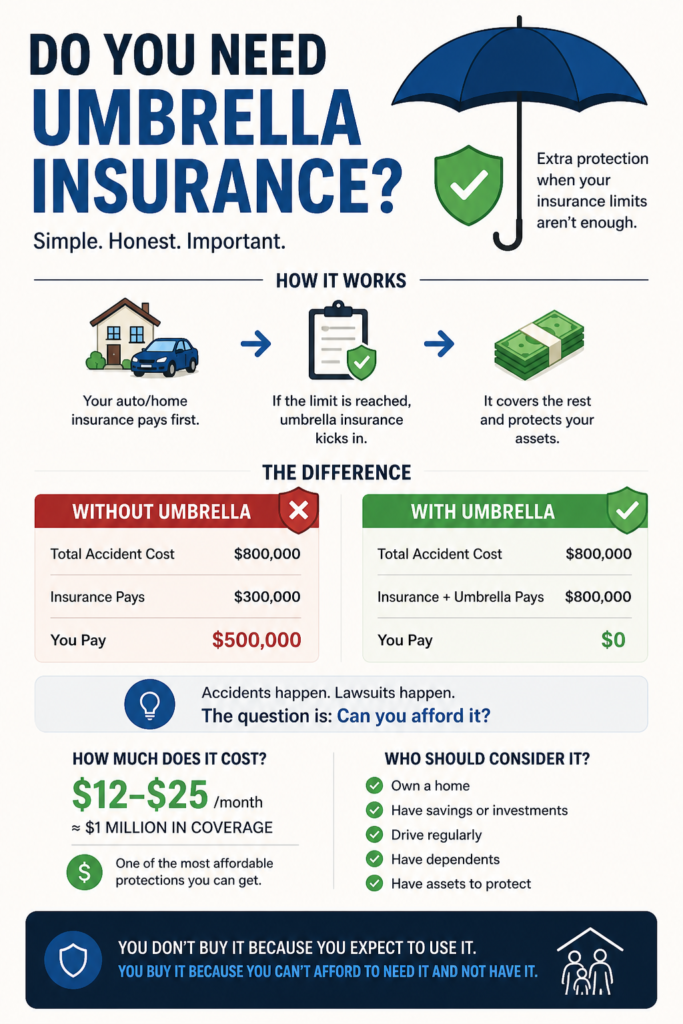

Umbrella insurance is coverage that kicks in when your main insurance runs out.

Simple as that.

- Your auto/home insurance pays first

- The limit is reached

- The umbrella covers the rest

It exists to cover the “gap.”

And that gap is exactly where people get financially crushed.

This type of insurance was created specifically to protect against high legal costs and liability claims that exceed standard policies.

The real problem: costs in the U.S. are out of control

Here’s what most people underestimate:

The U.S. is one of the most litigious countries in the world.

And that’s not just opinion, it’s a trend.

- Legal costs and settlements are rising

- High-value court cases (“nuclear verdicts”) are becoming more common

- Insurers are paying more large claims

In fact, this increase is one reason insurance premiums are going up.

👉 Simple translation:

The risk isn’t just “something happening.”

The risk is how much it costs when it happens.

So how much does protection cost?

Here’s the most surprising part: Umbrella insurance is cheap.

- $1 million in coverage: about $150–$300 per year (based on sources like Compare.com)

- That’s roughly $12–$25 per month

- Each additional $1M costs about $75–$100/year

In other words:

You pay very little to protect yourself from very large losses.

And there’s more:

- Fewer than 20% of American households have this coverage

Which means most people are exposed without realizing it.

The practical difference (this is what matters)

Let’s go straight to a real scenario:

| Situation | Without Umbrella | With Umbrella |

|---|---|---|

| Total accident cost | $800,000 | $800,000 |

| Base insurance | $300,000 | $300,000 |

| Umbrella | $0 | $500,000 |

| You pay | $500,000 | $0 |

This isn’t theory. It’s basic math.

So why don’t more people have it?

The answer is simple: it feels unnecessary.

And here’s our direct opinion:

People underestimate large risks because they don’t happen every day.

But that mindset is dangerous.

Because:

- Probability → low

- Impact → extremely high

And smart financial decisions are based on impact, not just frequency.

Who should seriously consider umbrella insurance

You should take a close look if you:

- Own a home

- Have more than ~$50k–$100k in assets

- Invest (stocks, 401k, etc.)

- Drive regularly

- Have children or dependents

Why? Because all of this increases:

- your exposure to risk

- what you stand to lose

And here’s an important detail:

Experts (including guidance commonly cited by outlets like Forbes) suggest your coverage should match — or exceed — your net worth.

When it does NOT make sense (full honesty)

Not everyone needs it.

If you:

- Don’t have meaningful assets

- Are just starting financially

- Have low exposure (e.g., rarely drive)

It may not be a priority right now. But be careful:

This changes fast.

Most people only think about it after they already have something to lose.

The detail almost no one tells you

Umbrella insurance is not plug-and-play.

To get it, you usually need:

- High-limit auto insurance (e.g., $250k/$500k)

- Active homeowners insurance

In other words: it’s an extra layer, not a replacement.

Where to get it (U.S.)

Major insurers include:

- State Farm

- Allstate

- GEICO

- Progressive

They all offer similar products.

But here’s the critical point:

The biggest mistake isn’t choosing the wrong company. It’s not understanding what your policy actually covers.

The truth most people won’t say (strong opinion)

Let’s be direct:

👉 Umbrella insurance is not necessary for everyone.

👉 But completely ignoring it can be a costly mistake.

Because:

- It’s one of the cheapest coverages per dollar of protection

- It protects exactly the kind of risk that can financially destroy you

- The U.S. legal environment is getting more expensive

And here’s the line that sums it up:

You don’t buy umbrella insurance because you expect to use it.

You buy it because you can’t afford to need it and not have it.

Quick Summary

☂️ Umbrella Insurance — Quick Summary

- Extra protection above your insurance limits

- Costs ~$12–$25/month

- Covers large lawsuits and liability claims

- Best for people with assets

Take it with you

Save this image to your phone and keep key information about umbrella coverage at your fingertips.

Conclusion (no fluff)

If you want a simple answer:

👉 Have assets? Seriously consider it.

👉 Don’t have them yet? Focus on building first.

But don’t fall into this trap:

“That will never happen to me.”

Because the problem isn’t if it happens.

👉 It’s how big the damage is when it does.

FAQ — Umbrella Insurance (U.S.)

Related content

Are You Overexposed to Your Employer’s Stock?

Learn how to manage employer stock risk, avoid overexposure, and build a diversified portfolio for long-term financial stability.

Keep reading * You will remain on the current websiteI have been a content producer for over 10 years, specializing in online writing across a wide range of topics—particularly finance, health, and human behavior. I’m an expert in SEO-driven writing and cultural research.