APR vs Loan Fees: what costs more?

Compare APR and loan fees the smart way. Learn which borrowing costs matter most before choosing a personal loan.

How to Compare the Real Cost of a Personal Loan

If you live in the United States and have ever searched for a personal loan online, you have probably seen something like this:

💸 Low APR

“Only 8.99% APR”

📄 Hidden Fee

“Origination fee may apply”

🤔 Confusion

Which costs more?

You are thinking like someone who actually understands credit.

Because here is the truth many lenders would rather you ignore:

APR alone does not tell the full story.

And the opposite is also true:

Origination fees alone can also be misleading. The only smart question is:

What is the real total cost of this loan?

And here is this site’s clear position: Most Americans compare loans the wrong way.

According to the Federal Reserve Bank of New York Household Debt Report, total U.S. household debt now exceeds $18 trillion, showing how small structural borrowing-cost differences create massive long-term financial consequences.

📉 Lower APR does not always mean a cheaper loan.

Total borrowing cost is what matters.

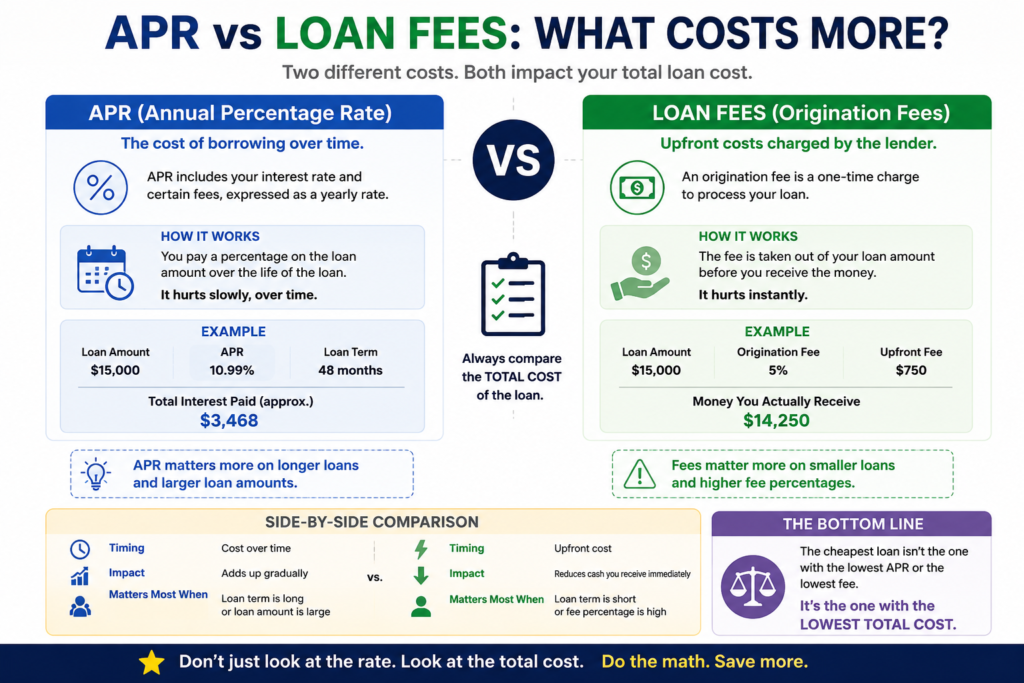

What is APR?

APR stands for:

Annual Percentage Rate

It reflects the annualized borrowing cost, including interest and sometimes certain fees.

According to the Consumer Financial Protection Bureau, APR was created to standardize credit comparisons.

Sounds simple. But there is a catch:

Not every fee appears the way you expect.

According to Federal Reserve Consumer Credit Release (G.19) data, average consumer borrowing costs remain elevated due to monetary tightening cycles.

That means even a 2–3 percentage point APR difference can translate into hundreds or thousands of dollars over time.

What is an origination fee?

It is a charge lenders apply to process your loan.

Typical ranges:

- 1%

- 3%

- 5%

- Up to 10% with aggressive online lenders

Example:

- Loan amount: $10,000

- Origination fee: 5%

- You receive: $9,500

But you may still pay interest on the full $10,000.

You can literally pay for money you never received.

According to official CFPB guidance, consumers often underestimate this cost because they focus only on APR.

The psychological trick lenders use

Your brain loves smaller numbers.

Look:

Offer A

- APR: 9.9%

- Fee: 6%

Offer B

- APR: 13.5%

- Fee: 0%

Most people choose A. Because 9.9 feels better.

But depending on the term, it may cost more.

That is marketing psychology.

Case example: Emily, 33, Dallas

She needs $15,000 to consolidate debt. She gets two offers:

| Offer | APR | Fee | Net Funds Received | Estimated Total Cost |

|---|---|---|---|---|

| A | 8.99% | 6% | $14,100 | ~$17,950 |

| B | 11.75% | 0% | $15,000 | ~$17,300 |

Result: Lower APR. Higher cost.

This happens constantly.

💡 Financial reality:

A lender can advertise a lower APR and still charge more overall.

Why fintech lenders love fees

Because upfront fees:

✅ Generate immediate revenue

✅ Reduce lender risk

✅ Feel smaller to borrowers

According to the Bank for International Settlements, fintech lenders have grown rapidly by combining competitive APRs with structural fees.

Translation: The ad looks cheap.

The math often is not.

When APR matters more

APR dominates when:

- Loan terms are long

- Balances are high

- Fees are low

Example:

$30,000 for 72 months

| APR | Approximate Interest Cost |

|---|---|

| 8% | ~$6,500 |

| 10% | ~$8,200 |

| 12% | ~$10,000 |

Here, APR is king.

When fees hurt more

Fees matter most when:

- Terms are short

- Loan amounts are small

- Percentage fees are high

Example:

$5,000 loan with 8% fee

Immediate loss:

$400

That is an instant cash-flow hit.

📈 APR hurts slowly

Long-term accumulation

⚡ Fees hurt instantly

Immediate cash reduction

How to compare loans correctly

Stop looking at ads.

Ask three questions:

- How much money actually hits your account?

- How much will you repay in total?

- What is the effective borrowing cost?

- Formula:

(Total Paid − Net Funds Received) ÷ Net Funds Received

Almost nobody calculates this.

Smart borrowers do.

The mistake most Americans make

According to FDIC consumer finance surveys, financially inexperienced borrowers compare credit using only monthly payments.

Financially sophisticated borrowers compare:

- Total cost

- Term length

- Effective borrowing cost

That difference changes everything.

Red flags

🚩 Guaranteed approval

🚩 Bad credit? No worries

🚩 Upfront payment requests

🚩 High-pressure urgency

The FTC frequently warns about these lending scams.

Major market players

SoFi

Pros:

Great UX

Competitive pricing

Cons:

Selective underwriting

Upgrade

Pros:

Wider approvals

Cons:

Fees can be heavy

LendingClub

Pros:

Established platform

Cons:

Cost varies significantly

Discover

Pros:

No origination fee

Cons:

Tougher approval standards

Our honest view:

Discover is usually more transparent.

Transparency saves money.

🔥 Smart rule:

If fees exceed 5%, compare much harder.

The 5% rule

If origination fees exceed 5%: Investigate aggressively.

Ask: Why is it so high?

Does APR justify it?

Is there a zero-fee alternative?

Often, there is.

The classic mistake

Average borrower asks:

“Can I afford the monthly payment?”

Smart borrower asks:

“What is my total cost of capital?”

That is the right question. Always.

💭 The right question is not:

“What is the monthly payment?”

👉 It is:

“What is the total borrowing cost?”

Final checklist

✓ APR

✓ Origination fee

✓ Net funds received

✓ Total repayment

✓ Prepayment penalties

✓ Fixed or variable rate

Without these:

You are borrowing blind. And blind borrowing is expensive.

The data that explains everything

According to FINRA’s National Financial Capability Study, many American adults struggle to compare combined financial costs involving both rates and fees.

That is exactly why so many borrowers choose the wrong loan.

Conclusion

Loans in America are not expensive only because of interest. They are expensive because consumers focus on the wrong number.

APR matters. Fees matter.

But neither tells the whole story alone.

The truth is simple:

The cheapest loan is the one with the lowest real total borrowing cost — not the lowest advertised number.

If you understand that, you are already comparing credit better than most Americans.

And over time, that will save you serious money.

Compare now

See a clear visual guide to compare different loan costs and understand which fees impact your borrowing the most.

Frequently Asked Questions

Related content

Smarter Emergency Loan Options

Explore safer alternatives to payday loans and learn smarter ways to handle emergency cash needs fast.

Keep reading * You will remain on the current websiteI have been a content producer for over 10 years, specializing in online writing across a wide range of topics—particularly finance, health, and human behavior. I’m an expert in SEO-driven writing and cultural research.