Fast Cash Isn’t Free: Smarter Emergency Loan Options

Explore safer alternatives to payday loans and learn smarter ways to handle emergency cash needs fast.

Why Most Americans Choose the Wrong Emergency Loan

If you live in the United States and have ever typed “need money fast” into Google, you have probably seen the same scenario:

- Payday loans

- Cash advance

- “Instant approval”

- “Money in minutes”

Most emergency loans do not actually solve the financial problem.

They simply push the problem a few weeks forward — with interest attached.

According to the Consumer Financial Protection Bureau, many payday loans end up trapped in renewal cycles, where borrowers take out a new loan to pay off the previous one.

You are not buying time.

You are renting financial desperation.

See how to break this cycle.

The real problem is not lack of money

In most cases, the real issue is:

⚡ Urgency

The bill is due TODAY

🧠 Lack of information

The person only knows payday loans

📉 Emotional decision-making

Fixing it fast > fixing it correctly

And the market knows that — which is why it keeps offering expensive “quick solutions.”

How expensive is “fast money” in the U.S.?

According to the Consumer Financial Protection Bureau:

- Payday loans often equal APRs of 300%–400%+

- Many loans must be repaid within 2 weeks

- A large percentage of borrowers renew or “roll over” the debt

Real example

| Amount borrowed | Fee | Repayment |

|---|---|---|

| $300 | $45 fee | $345 in ~14 days |

At first, it may not look terrible.

But annualized?

APR can exceed 390%.

🚨 The reality:

You borrow $300 to solve a small problem and may end up creating a much larger financial one.

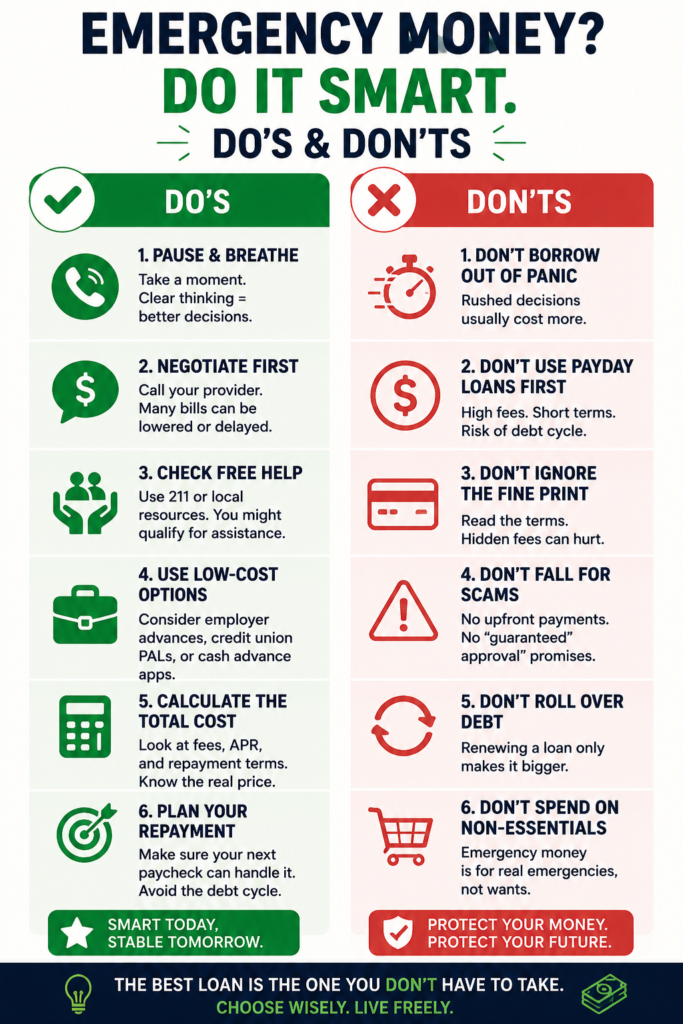

Before borrowing money: ask these 3 questions

1. Is the problem truly urgent?

Many bills can be negotiated.

2. Is there a free alternative?

Local assistance, employer advances, family support.

3. Does this solve the issue or just delay it?

If your next paycheck is already committed, be careful.

Alternative #1 — Cash Advance Apps

Apps like Dave, EarnIn, Brigit, and MoneyLion have basically become the new payday loans — but with some important differences.

How they work

You receive part of your paycheck before payday.

| Feature | Average |

|---|---|

| Amount | $50–$500 |

| Interest | Usually 0% |

| Fees | Transfer + subscription |

Advantages

The hidden problem

Here is the important part: 👉 Automatic repayment.

The app pulls the money directly from your next paycheck.

Common result:

You run out of money again → use the app again → create dependency.

According to the Consumer Financial Protection Bureau, short-term debt cycles are one of the biggest risks in emergency borrowing.

Alternative #2 — Employer Paycheck Advance

This one is EXTREMELY underrated.

Many American companies now offer:

- paycheck advance

- earned wage access

- salary advance

Popular platforms include:

- DailyPay

- Payactiv

- Even

Why does this matter?

Because:

The issue?

Many people feel embarrassed asking HR about it.

But here is the practical perspective: Paying 0% is better than paying 400%.

Alternative #3 — Credit Union PALs

According to the National Credit Union Administration, credit unions may offer:

Payday Alternative Loans (PALs)

Structure

| Metric | PAL |

|---|---|

| Maximum APR | 28% |

| Amount | up to ~$2,000 |

| Term | up to 12 months |

📉 Compare:

28% APR vs 400%+ APR

That changes everything.

PALs are:

- regulated

- installment-based

- significantly less aggressive

Alternative #4 — Free Assistance Programs

This is probably the most overlooked option.

And one of the most powerful.

Common U.S. programs

| Program | Assistance |

|---|---|

| 211 | general assistance |

| LIHEAP | energy bills |

| SNAP | food assistance |

| Food banks | groceries |

| Rental assistance | housing support |

According to the United Way, the 211 system receives millions of annual contacts related to financial hardship.

💡 Important insight:

If you borrow money before checking free assistance programs, you may be leaving money on the table.

Alternative #5 — Personal Loans

If the amount needed is larger:

- medical emergency

- car repair

- moving expenses

- debt consolidation

- payday loans become even more dangerous.

Personal loans usually offer

| Feature | Average |

|---|---|

| Installments | Yes |

| APR | Much lower |

| Term | Longer |

But be careful

According to the Federal Trade Commission:

- loan scams have increased

- “guaranteed approval” is a warning sign

- upfront fees are dangerous

🚩 Red flags:

- “Guaranteed approval”

- Requests for upfront payment

- Urgent pressure tactics

- No clear contract

The invisible cost of financial desperation

Here is a point that rarely gets discussed:

Financial emergencies do not only destroy money.

They damage:

- cash flow

- credit

- emotional stability

- decision-making ability

And that leads to worse decisions

According to behavioral finance research from the National Bureau of Economic Research:

Financial stress reduces decision quality.

In other words: the more desperate someone becomes, the worse their decisions tend to be.

The killer tip (original)

The “72-Hour Financial Rule”

If the emergency does not involve:

- immediate medical risk

- housing loss

- immediate job loss

wait 72 hours before borrowing money.

Why does this work?

Because:

Side-by-side comparison

| Option | Cost | Speed | Risk |

|---|---|---|---|

| Payday loan | Extremely high | Immediate | Very high |

| Cash advance app | Low–medium | Very fast | Medium |

| Employer advance | Very low | Fast | Low |

| PAL (credit union) | Low | Medium | Low |

| Assistance programs | Zero | Variable | None |

The biggest lie in the market

“Fast cash solves emergencies.” Not exactly.

Fast money solves short-term urgency.

But high interest creates long-term problems.

💭 The right question is not:

“How fast can I get money?”

👉 It is:

“What will this cost me in 30, 60, and 90 days?”

The right question is not:

“How fast can I get money?”

👉 It is:

“What will this cost me in 30, 60, and 90 days?”

Practical strategy (what to do TODAY)

If you are facing an emergency right now:

Correct order:

- Negotiate the bill

- Check free assistance programs

- Employer advance

- Cash advance app

- Credit union PAL

- Personal loan

Payday loans should be close to the last resort.

Take this with you

Emergency cash can help — or trap you. Save this guide and make smarter borrowing decisions when money gets tight.

Conclusion (without sugarcoating)

The fast cash industry exists because:

urgency sells

desperation converts

speed feels like a solution

But financial speed is usually expensive.

Our clear position: Not every emergency loan is bad.

But borrowing without a strategy almost always becomes a problem.

And here is the sentence that summarizes everything:

“The fastest money is rarely the cheapest money.”

FAQ

Related content

Do You Need Umbrella Insurance?

Learn how umbrella insurance works, costs, and when it protects your assets beyond standard coverage.

Keep reading * You will remain on the current websiteI have been a content producer for over 10 years, specializing in online writing across a wide range of topics—particularly finance, health, and human behavior. I’m an expert in SEO-driven writing and cultural research.